A travel merchant account helps you manage all your transactions. It also allows you to integrate into your booking software; plus, there are more features that you get to process payments in a secure environment.

Virtual Merchant Payment Terminal

This is a web-based system that allows you to view processed payments in real-time. You can access it using any web browser, and the transactions are conducted over a secure and encrypted connection.

Customers get receipts for their payments via email once the transaction is complete. You can also handle installments and recurring payments online. It also accepts different payment methods, including gift cards, electronic checks, and credit and debit cards.

Loyalty Programs

With a travel merchant account, you are able to reward your loyal travel customers. You can personalize your loyalty program for customers basing on their behavior. A loyalty program can offer free products or discounts on certain tour or travel packages.

Also, you can make gift cards part of your program. With these cards, you can simply load them with any dollar amount and present them to your customers. Plus, they’re re-loadable and offer a great way of advertising. These programs can go a long way in boosting your customer’s loyalty.

Trams & Sabre Integration

If you’re using Sabre Travel Network for agency services, you can easily integrate your account into Sabre to improve your travel options. This integration allows you to provide convenient payment methods for customers searching for cruise lines, hotel properties, car rental services, and airlines.

Also, for those using Trams for accounting and reporting, NTC travel merchant account lets you make a simple integration. In the long run, you are able to focus on growing your travel agency and offer quality services to your clients.

Mobile Processing

Accepts payments fast and on-the-go with mobile processing solutions that are PCI compliant. With this service, you only need to use a mobile device card reader to swipe cards.

Mobile payment processing allows you to use your own iOS or Android device with a free mobile app which you can integrate with your account to manage transactions.

Offering a convenient and smooth payment methods to your clients is one of the ways to grow your business. National Transaction Corporation merchant account, offers secured travel payment processing services e-Pay, to process your payments; with no delays and at a very competitive rates.

Also, you can accept payments from anywhere and get 100 percent funding. Faster deposits for bookings, which can occur as quick as the next business day.

To speak to our travel payment consultant, call now 888-996-2273

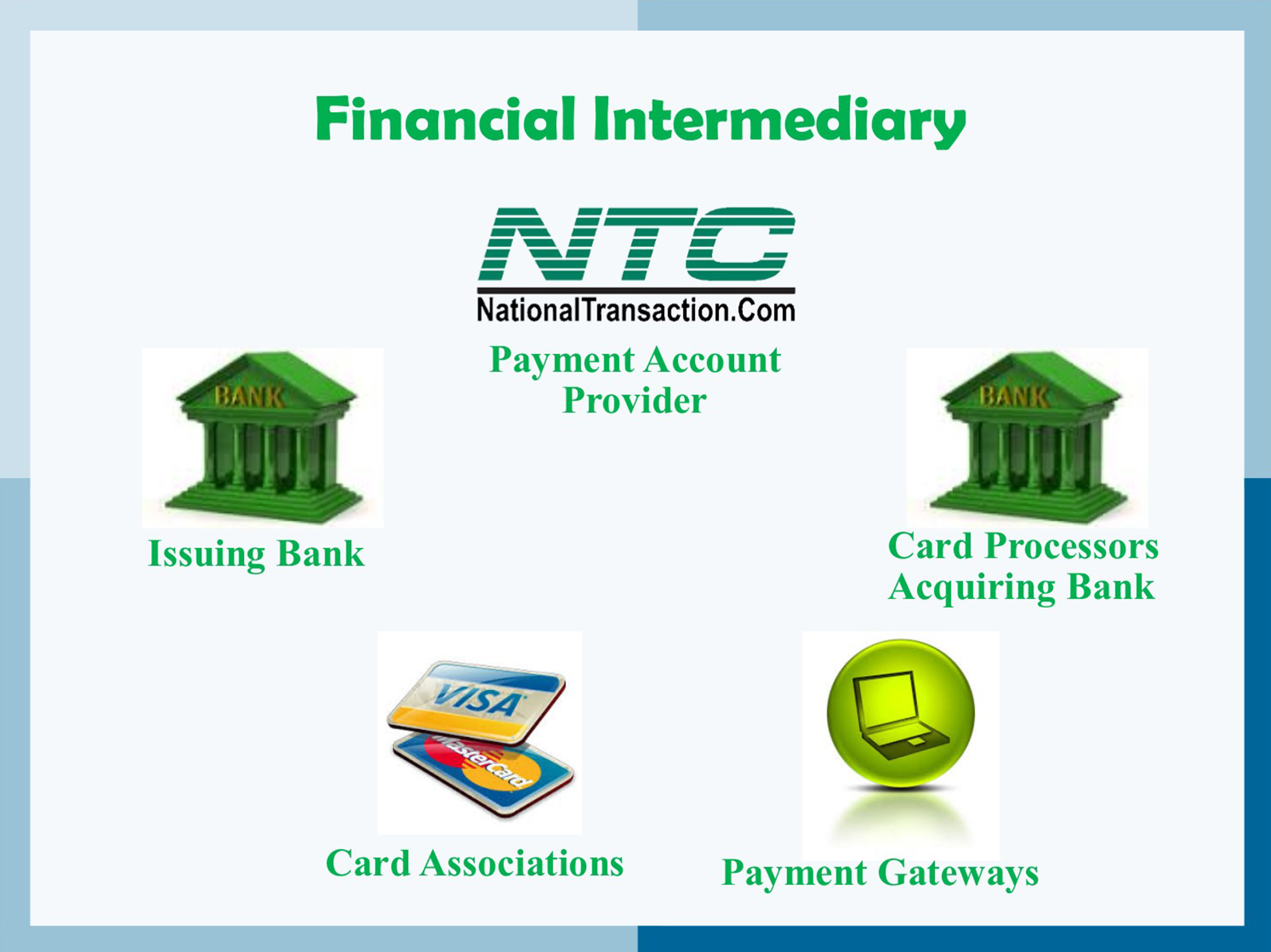

Financial intermediary between a customer and merchant include:

Card Associations – Visa, MasterCard, and American Express.

Card Issuing Banks – are thefinancial institutions affiliated with the card association brands and provides credit or debit cards directly to customers.

Card Processors – alsoknown as Acquirer or Acquiring Banks. They pass batch information and authorization requests so that merchant can complete transactions in their businesses. These institutions are the link between payment account providers and card associations.

Payment Account Providers – are companies like NTC that manage credit card processing, usually through the help of a Card processor also known as Acquiring Banks.

Payment Gateways: These are special portals that route transactions to a card processor or acquirer.

Learn more about the full range of payment capabilities offered by Converge, an omni-commerce platform that lets you accept payments your way. Online, In-Store and On the Go!

Accept a full range of payment methods:

Credit Cards

Debit Cards

Electronic Checks

Gift Cards

Electronic Benefit Transfer (EBT)

Cash

Advanced features also include:

Available enhanced security features, including EMV, encryption and tokenization

Detailed reporting with up to 12 months of data storage

Customizable payment screens

User permission management for up to 5,000 users

National Transaction Corporation accept payments wherever you are with security while having a peace of mind for you and your customers. Furthermore, flexible solutions that empower your business growth in addition to world class support for complex integrations and answers to your toughest questions. Let our payment specialist find the right solution for your electronic payment needs. We offer transparent pricing and services that work with your existing technology to provide a low cost automated billing and collection solution.

Call now at 888-996-2273 and get a FREE Rate Review!

Credit card processing involves three separate cost components:

For vendors who choose to accept this type of payment, from customers for goods or services.

The same cost components apply to debit cards. Only one cost component is negotiable.

The first component is an interchange fee, which is payable to the card holder’s issuing bank. It is a combination of a transaction volume percentage fee and a flat-rate transaction fee. Interchange fees are collectively agreed upon through Visa and MasterCard by a card’s issuing bank and are fixed costs.

Interchange fees take into consideration various information about a card. Types of cardsinclude debit and credit, while categories of cards refer to commercial and reward cards. Processing methods include whether a card is swiped or manually keyed. Swiping a card is usually more economical for vendors.

The second component is an assessment fee, charged by the card’s brand holder. Brand holders include Visa, MasterCard and Discover. Assessment fees are also fixed costs. Additionally, Visa charges a monthly fee.

The final charge is known as a processing fee. Processing fees vary among processors and is negotiable. Vendors are charged a processing fee, which can cause a difference in cost from one vendor to another.

Let’s talk about your money, and how to make more of it. Today money is taking on a new form. It’s digital, it’s electronic and it’s everywhere and anywhere 24/7/365.

Payment acceptance is key to making more money. You don’t make more money by not accepting a transaction, and making the experience convenient and safe to your customer can bring loyalty.

Let’s break down a transaction.

Cash, but that would mean that the customer has to be in front of you. You could take checks, those are safe to mail, but then you don’t have your money until you drive to the bank and cash or deposit the check.

So how do we easily and securely transfer funds for a transaction? The answer lies in digital or electronic payments. Accepting credit cards, debit cards, ebt cards or even gift & loyalty cards and electronic checks. These provide secure and convenient ways to complete transactions for your customers. If you want to make more money, make it easy for customers to spend it while making it faster for you to receive it. That’s where a merchant account comes in.

A merchant account allows you to deposit funds directly into your bank account in as little as a few hours. Whether the customer swipes their card into your smartphone, calls it in over the phone or keys it into your web site, just having a merchant account can be a huge advantage over competitors.

It allows you to conduct transactions in more ways than cash or checks alone. Transactions are recorded automatically and can easily be reconciled for both customer and merchant. Most importantly it widens the opportunities to conduct sales to the widest customer audience possible.

No matter what you sell or how you sell it, the sale is only complete once the funds are transferred from one party to the other.

It’s important to recognize your missed opportunities. Could accepting electronic payments help increase your revenue stream? We’re here to help you make more money, let us show you the many ways we can do just that. Let’s talk, 888-996-CARD (2273)

Merchants need to stay competitive by offering the most modern forms of electronic payment processing technology to satisfy customers, because, in today’s world of smartphones and one-the-go payments, consumers have options in how they conduct their transactions. With proper education on the types of payment options, merchants can make the right decision for their business.

NTC is here to discuss that payment options.

EMV – or Europay, MasterCard, Visa is a fraud-reducing technology to protect card issuers, merchants, and consumers from counterfeit or stolen cards. The customer inserts or dips the chip card into the EMV terminal, rather than swiping the card at the point of sale. A one-time-use code is created for that transaction. This code makes it virtually impossible for anyone to duplicate, leaving customers safer from fraud.

NFC – stands for near field communication is a method of contactless data exchange between two electronic devices. NFC is used in mobile wallets such as Apple Pay, Android Pay, and Samsung Pay. More and more consumers leaning towards mobile wallets, merchants should be prepared to accept NFC payments by incorporating NFC-enabled equipment.

Virtual Merchant Mobile Payments – Mobile Payments are popular, you can take payments anywhere. Ideal for retail, restaurant and service businesses of any size. Accept payments your way online, in-store and on the go. Anytime and anywhere.

Offers flexibility you want with the payment security you and your customer need:

Accept credit and debit cards, including mag stripe, chip cards, and contactless payments/NFC, like Apple Pay and other mobile wallets.

Calculate discounts, taxes, and tips automatically.

Email customer receipts.

Help protect cardholder data with an encrypted, chip card device.

Record cash transactions.

Use your own smartphone or tablet (works with most IOS and Android mobile devices).

Check out NTC’s electronic payment solutions that are EMV-capable, NFC-enabled and mobile wallet ready.

The roll out for EMV PIN Debit and Tip Adjust functionalities for the Ingenico Telium POS terminals through a gradual download process begins July 24, 2016. Customers will receive an automatic download following the July release date, or they can go to their appropriate website for instructions to manually update their terminal file.

What to Expect

EMV PIN Debit support for Visa, MasterCard, and Discover common Debit AIDs. Note that customers will see new prompts based on how card issuers configure EMV-enabled debit cards.

Tip Adjust functionality on the restaurant application.The tip at the time-of-sale prompt will be on by default and will work as it always has. However, if this prompt is bypassed, a blank tip line will print on the receipt. This allows consumers to write the tip amount on the receipt and our customers can adjust as needed.

Tip Adjust is supported on credit card transactions only, including magnetic stripe, EMV, key-entered and contactless.

It’s important for merchants to understand the basic of how a credit card terminal works. It is the channel through which the process flows and the merchants can choose the right one for their processing needs, whether they use a point-of-sale (POS) countertop model, a cardreader that attaches to a smartphone or mobile device, a sleek handheld version for wireless processing or a virtual terminal for e-commerce transactions.

A credit card terminal’s function is to retrieve the account data stored on the payment card’s EMV microchip or a magnetic stripe and pass it along to the payment processing company (also known as merchant account provider).

For card-not-present (CNP) – mail order, telephone order and online transactions – the merchant enters the information manually using a keypad on the terminal, or the e-commerce shopper enters it on the website’s payment page. The back half of the process remains the same.

The actual data transmission goes from the terminal through a phoneline or Internet connection to a Payment Processing Company, which routes it to the bank that issued the credit card for authorization.

In card-present transactions where the card and cardholder are physically present, the card is connected to the reader housed in the POS terminal. The data is captured and transmitted electronically to the merchant account provider, who handles the authorization process with the issuing bank and credit card networks.

A POS retail terminal with a phone or Internet connection works best in a traditional retail setting that deals exclusively in card present transactions. For a business with a mobile sales, a mobile credit card processing option like Virtual Merchant Converge Mobile relies on a downloadable app to transform a smartphone or tablet into a credit card terminal equipped with a USB cardreader.

Wireless Terminals are compact, allowing you to accept credit cards in the field without relying on a phone connection. If you process debit cards, you’ll need a PIN pad in addition to your terminal so cardholders can enter their personal identification number to complete the sale.

Selecting the right terminal for your credit card processing needs depends largely on the type of business you run and the sorts of transactions you process. Terminals are highly specialized and provide different services. At National Transaction we offer a broad range of terminals with NFC (near field communication) Capability to accept Apple Pay, Android Pay and other NFC/Contactless payment transactions at your business. An informed business decision benefits your bottom line. Start accepting credit cards today with National Transaction.

Adoption of EMV technology in the U.S is important, because it provides protection against losses from counterfeit cards.

EMV, or chip cards, are the standard for secure point-of-sale (POS) transactions. Unlike magnetic stripe cards, chip cards are very difficult to counterfeit because of an embedded microchip that exchanges unique, dynamic data with a terminal each time it’s used.

To encourage the timely adoption of EMV, the leading payment networks have implemented an EMV Fraud Liability Shift that began in October 2015.

Both parties, card issuer and the merchant need to invest with EMV technology. If only one party has adopted EMV technology, the party that didn’t make the investment will be held liable.

For the card issuer, they came out with the chip cards, where all credit and debit cards have this security chips that are harder to counterfeit than magnetic strips.

For the merchant, an EMV capable terminals or POS hardware that can take advantage of the card’s security chip is needed.

With any new technology, there is a learning curve, and here are the things that you need to know.

For cardholders – with a chip card instead of swiping your card, you are going to do what is called card dipping; by inserting your card face-up and chip-first into the terminal slot. Wait and follow the terminal prompts, and only remove your card once the transaction is complete.

If you did a swipe on a chip card, an EMV-enabled terminal should prompt you to insert the card instead. If the terminal is not enabled for chip, you can still be able to swipe your card.

Employees will benefit from training – Once a merchant enables their EMV terminals, it is important to train your staff with talking points about why chip cards benefit consumers with greater security, and how they are used by helping customers with the new checkout process.

New mobile payment methods leverage both EMV and NFC, so the industry is now seeing greater interest in mobile payments among merchants and consumers.

There’s a lot of resources out there to help businesses make the transition with this EMV technology.

With the EMV liability shift that takes effect in October 2015, how much you’ll be affected depends on how you process credit card payments.

For Card Present Transactions

If you use POS hardware or terminal that you need to swipe the credit card, then you’ll be facing the same EMV environment as retailers. October 1st is the start of the liability shift for fraudulent charges made with the card present transactions. The party who hasn’t made an investment in EMV security features will be liable.

For the card issuer, they need to invest in EMV security features, that’s why they came out with the chip cards, where all credit and debit cards have this security chips that are harder to counterfeit than magnetic strips.

For the merchant, they need to invest in EMV capable terminals or POS hardware that can take advantage of the card’s security chip.

If both parties have made the investment, then liability will be resolved in a similar manner to how it was before the shift. However, if only one party has adopted EMV technology, the party that didn’t make the investment will be held liable.

For Card Not Present Transaction (CNP)

If you process credit cards online, over the phone, or through an online payment gateway integrated, the new EMV standards won’t directly change the way you do business. You’ll still be processing EMV cards based on the customer’s credit card number.

Chances are Card-Not-Present transactions will experience an increase in fraud. Because of the EMV-technology in the Card Present Transaction, fraudster will likely turn their attention to the next target which is CNP,

but payment gateways and banks concerned about the vulnerabilities, will begin to adopt new standards to minimize their exposure.

If you’re processing CNP transactions stay up-to-date on the newest security developments, online security standards find more effective ways to navigate the new credit card security frontier.